Dec 7

Trump is beginning to appease China. See Thomas Rogan and also Scott Bessent’s comments to Andrew Ross Sorkin at DealBook. Bessent said China is an ally of the United States.

https://www.washingtonexaminer.com/opinion/beltway-confidential/3907486/trump-new-weakness-on-china/

Russia is engaging in asymmetric war against Europe. Drones are plaguing German airspace especially over its airfields. The French military responded with its air defense systems when drones were detected over its nuclear submarine base.

I am pounding the table on European defense stocks. Rolls Royce, Rheinmettal, BAE Systems and Airbus SE are my top picks.

US reliance on China’s rare earths is set to decline. This is great news.

@The Kobeissi Letter: The US is now on track to meet ~94% of its rare earth demand from domestic sources by 2030. This percentage is expected to more than quadruple from the 20% seen in 2024. By comparison, the rest of the world will only meet 38% of demand locally by 2030, up from 18% last year.

Overall, China is expected to supply ~60% of the world’s rare earth elements used to produce high-performance magnets by 2030.

However, Western economies will still rely on China for 91% of heavy rare earths processing through 2030, down from 99% in 2024, according to Benchmark Mineral Intelligence.

Rare earths are more strategic now than ever.

The Administration should be applauded for the new fuel efficiency standards. The new regulations will lead to more very small cars on the roads in the United States. See below under Economics.

Markets and Stocks

Momentum is positive. On Friday the S&P 500 closed 0.19% higher at 6,870.40, putting the index about 0.7% off its intraday record. Friday also marked its ninth positive session in 10. The Nasdaq Composite increased 0.31% to settle at 23,578.13.

The bull market is intact.

I want to highlight Rolls Royce, see below for more, and the largest banks: GS, JPM, BAC and MS. They act great. The wind is at their back.

In addition, for high risk tolerant traders, I like FLG, HOOD and CDE. See comments on silver below.

The Fed will cut on Wednesday but Powell’s tone will be hawkish in his post meeting press briefing.

Inflation is not out of control. The economy is growing at around 2.5% on a trend basis. Q3 growth was above trend, Q4 growth is expected to be in the range of 1.5-2%.

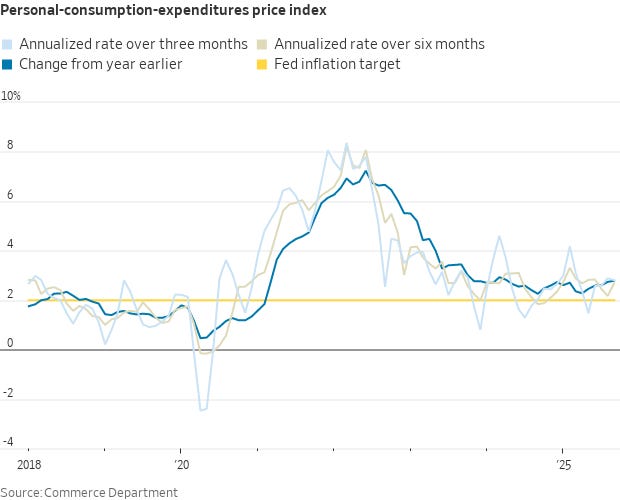

@Nick Timiraos Headline PCE printed at +0.27% in September, bringing the 12-month change to 2.8%. It was 2.7% in August and 2.3% in Sept. 2024

3-month annualized PCE inflation was 2.8% in Sept, and 6-month annualized PCE inflation was 2.7%.

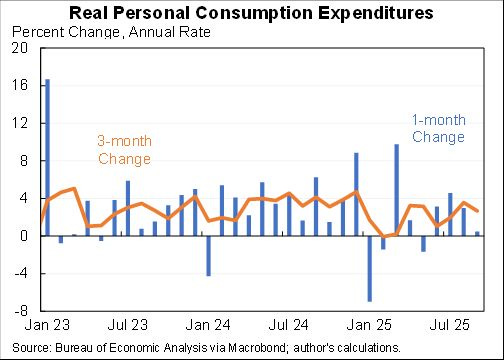

@Jason Furman On the real side of the economy, very little growth of consumer spending in September. But I wouldn’t worry much--overall has been very strong. Based on these numbers consumer spending grew at a 2.7% annual rate in Q3.

@Jason Furman In sum, inflation is 0.8pp above the Fed’s target. Consumer spending is consistent with Q3 GDP growth at 3%+ annual rate. Add to that fiscal expansion, wealth effect from asset price increases & the possibility of a bubble, and I just don’t get why the Fed is cutting next week.

Trump’s OBBB, deficit busting bill, will add fiscal stimulus in Q1 2026.

There are signs that hiring is picking up.

Goldman’s Rich Privorotsky: For all the focus on ADP (historically very noisy), the Indeed Hiring Lab data actually picked back up in the last couple of weeks (need more data). Notable was the re‑acceleration in open jobs in construction (see below). What if AI adoption is slower or less transformative in the near term... the labor market re‑accelerates... and inflation proves hotter in 2026? Not at all my base case but inversion an important part of the process.

Rolls Royce

The U.K. once had more nuclear power stations than the U.S., USSR and France combined but hasn’t completed a reactor since 1995.

Nuclear energy accounted for 14% of the U.K.’s power supply in 2023 but is targeting 25% by 2030.

The country is backing atomic projects big and small to “unlock a golden age of nuclear,” a spokesperson for the U.K. government’s Department for Energy Security and Net Zero told CNBC.

British company Rolls-Royce has been selected as the country’s preferred partner for SMRs, which are effectively containerized nuclear reactors designed to be manufactured in a factory. Many include passive cooling techniques, which supporters argue makes them safer and cheaper.

Silver

Silver touched a fresh record high and capped its second weekly gain as strong inflows to exchange-traded funds added more impetus to a scorching rally.

The white metal rose as much as 3.9% on Friday to an all-time high of $59.33 an ounce. Total additions to silver-backed ETFs in the four days through Thursday are already the highest for any full week since July, a strong indicator of investor appetite despite signs silver’s gains may be overdone. See Bloomberg.

Economics

Q4 GDP

The New York Fed Staff Nowcast for 2025:Q4 is 1.7%, with the 50% probability interval at [0.6, 3.0]% and the 80% interval at [-0.6, 4.1]%. The Staff Nowcast for 2026:Q1 is 2.2%.

News from this week’s data releases decreased the estimates for 2025:Q4 and 2026:Q1 by 0.6 and 0.5 percentage point, respectively.

Negative surprises from ADP employment and ISM manufacturing survey data drove the decrease for both quarters.

Political interference with the Fed leads to higher inflation and higher interest rates. Trump’s campaign for lower rates is harming the economy. Trump cares about himself and his family, nothing else.

This paper combines new data and a narrative approach to identify variation in political pressure on the Federal Reserve. From archival records, I build a data set of personal interactions between U.S. Presidents and Fed officials between 1933 and 2016.

Since personal interactions do not necessarily reflect political pressure, I develop a narrative identification strategy based on President Nixon’s pressure on Fed Chair Burns. I exploit this narrative through restrictions on a structural vector autoregression that includes the President-Fed interaction data.

I find that political pressure to ease monetary policy (i) increases the price level strongly and persistently, (ii) does not lead to positive effects on real economic activity, (iii) contributed to inflationary episodes outside of the Nixon era, and (iv) transmits differently from a typical monetary policy easing, by having a stronger effect on inflation expectations. Quantitatively, increasing political pressure by half as much as Nixon, for six months, raises the price level by about 7% over the following decade.

https://econweb.umd.edu/~drechsel/papers/drechsel_political_pressure_shocks.pdf

To let Americans buy smaller cars, Trump had to weaken fuel-efficiency standards. Does that sound crazy? Small cars, of course, have much higher fuel efficiency. Yet this is exactly how the Corporate Average Fuel Economy (CAFE) standards work.

Since 2011, fuel-economy targets scale with a vehicle’s “footprint” (wheelbase × track width). Big vehicles get lenient targets; small vehicles face demanding ones. A microcar that gets 40 MPG might be judged against a target of 50-60 MPG, while a full-size truck doing 20 MPG can satisfy a 22 MPG requirement.. The small car is clearly more efficient, yet it fails the rule that the truck passes.

The policy was meant to be fair to producers of large vehicles, but it rewards bloat. Make a car bigger and compliance gets easier. Add crash standards built around heavier vehicles and it’s obvious why the US market produces crossovers and trucks while smaller and much less expensive city-cars, familiar in Europe and Asia, never show up. At a press conference rolling back CAFE standards, Trump noted he’d seen small “kei” cars on his Asia trip—”very small, really cute”—and directed the Transportation Secretary to clear regulatory barriers so they could be built and sold in America.

Trump’s rollback—cutting the projected 2031 fleet average from roughly 50.4 MPG to 34.5 MPG—relaxes the math enough that microcars could comply again. Only Kafka would appreciate a fuel-economy system that makes small fuel-efficient cars hard to sell and giant trucks easy. Yet the looser rules remove a barrier to greener vehicles while also handing a windfall to big truck makers. A little less Kafka, a little more Tullock.