Sept 4

Sept 4

Democrats are crazy to propose raising corporate taxes.

U.S. households’ stock allocations have steadily inched up this year, according to JPMorgan estimates, and recently accounted for around 42% of their total financial assets. That is the most on record in data going back to 1952. See WSJ.

If the corporate tax rate is increased stocks will fall proportionately. Investors will not be happy.

Tax consumption not investment, production and innovation. .

I strongly oppose the blind pursuit of economic equality because achieving greater equality would make EVERYONE poorer. The private sector is more efficient than the public sector. By definition when economic equality is a major goal of government, private sector resources are confiscated by government. The government grows and the more productive private sector shrinks.

The far left argues that “investing” in lower income households leads to greater productivity by those households. The data says that too few households achieve high levels of productivity to compensate for diminished productivity by the most productive.

Basically government cannot change innate ability and government cannot change cultures of poverty. I say it ad nauseam, only the military can teach people to wake, make their bunks and “shine.”

@RadarHits VOLKSWAGEN PLANS TO CLOSE FACTORIES IN GERMANY - Bloomberg

@NetZeroWatch Car makers are rationing sales of petrol and hybrid vehicles in Britain to avoid hefty Net Zero fines as consumer demand for expensive EVs continues to wane.

The zero emission vehicle mandate will destroy our car industry. #CostOfNetZero

The push for green energy is destroying the European manufacturing sector.

Markets and Stocks

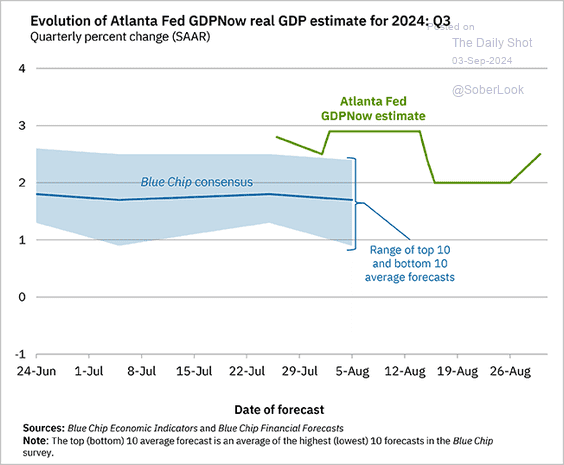

The market is in good shape. My year end target on the S&P 500 is 6,000, up around 7% from current levels. The economy is growing at a pretty good pace, say 2.5%. Inflation continues to fall. The Fed will begin a rate cutting cycle in two weeks. Earnings are growing.

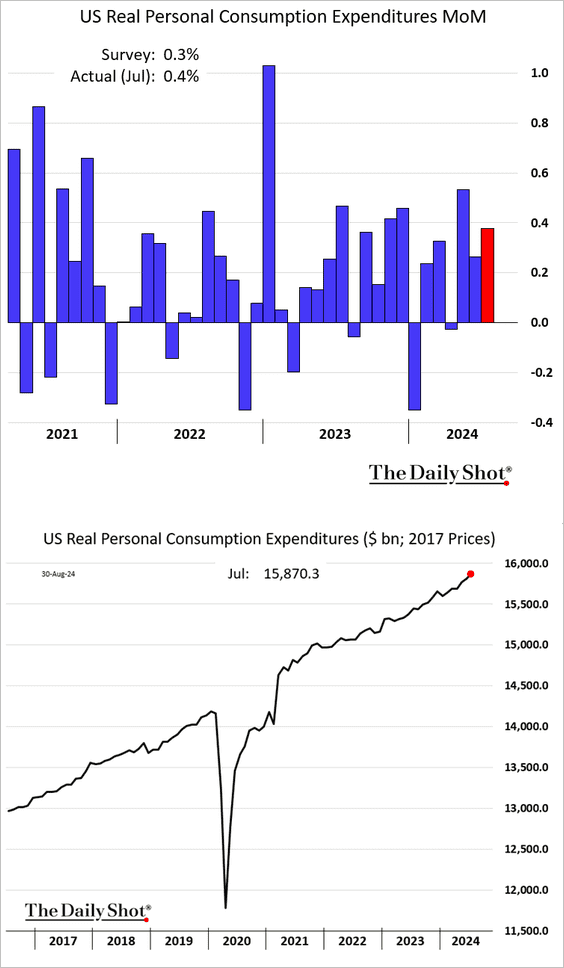

Consumer spending is strong.

As noted the economy is expanding.

The outlook for economic growth remains positive because real household income is growing.

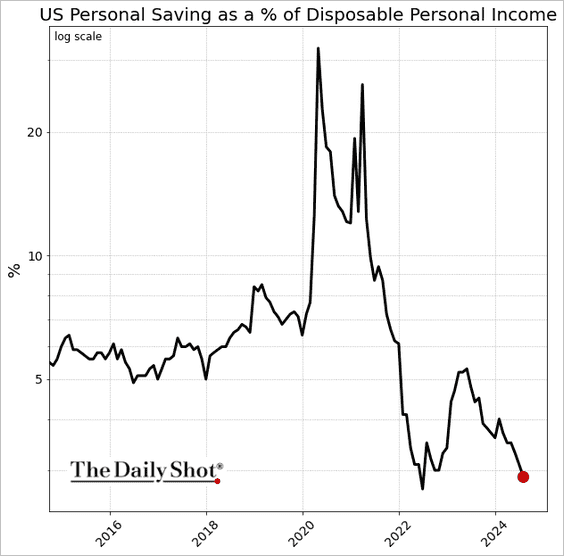

The savings rate is depressed but household balance sheets are in good shape because most households have ultra low mortgage payments.

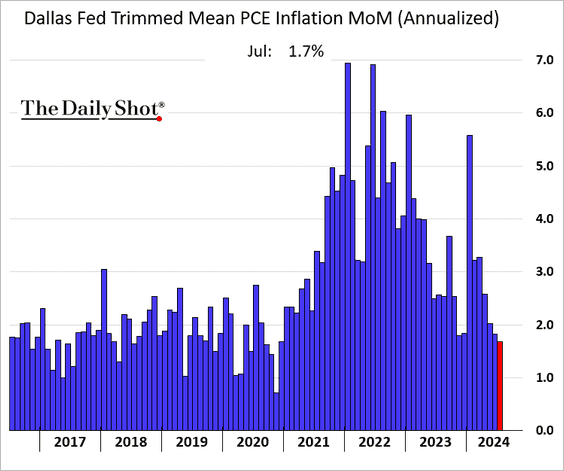

Inflation is falling sharply.

On Friday, the September employment report will signal both a resilient labor market and also a reasonably strong economy. Watch the hourly wage data.

And on Friday, Broadcom will report. I like AVGO.

Rolls Royce fell on Monday because of concerns about RR’s engines on Cathy Pacific planes. It turns out that the problem is with the fuel lines, not the engines. Rolls Royce rebounded yesterday. I like the stock. My target is 10.

I believe Eli Lilly is a must own stock. But it is expensive so tip toe into a position. I believe that LLY will be a great investment for the next decade.

People taking the key component of blockbuster weight loss drugs Ozempic and Wegovy were less likely to die of Covid-19 or suffer adverse effects from the virus, researchers found in a new study.

A crop of studies published by the Journal of the American College of Cardiology (JACC) on Friday indicate that semaglutide may have a wide range of health benefits beyond the previously identified reduction in risk of serious heart events such as heart attacks and strokes.

https://www.cnbc.com/2024/09/02/weight-loss-drugs-cut-covid-deaths.html

Businesses like TJX and Nordstrom Rack are taking market share.

Consumers are buying cheaper clothing, seemingly in response to high inflation, Bank of America Institute reported last month based on analysis of anonymized credit card data. Discount retail spending per household has been growing faster than overall retail spending since July 2022. “The market share for value apparel has increased nearly four percentage points for Gen Z and Millennials in the last year,” the institute said. The increase in the market share for cheaper clothing has been greater for lower- and middle-income consumers.

Economics

My views: have preferential rates for capital gains. Encourage investment and savings. But on death, tax capital gains without a stepped up basis. And reform estate taxes. The U.S. system of estate taxes is too generous.

For the very wealthy, tax cash flows as Jason Furman proposes. When the very wealthy borrow to maintain consumption without triggering tax liability, a cash flow or consumption tax would ensure that they, the very wealthy, do pay taxes. Everyone needs skin in the game and that includes both the very top and very bottom.

@jasonfurman I would do something like a Bradford X tax. Tax cash flows, don't tax normal return, but do it in a progressive manner. Within the current system, would tax accrued gains but at a lower rate. OR do something equivalent, like borrowing taxable & taxing at death.

Sociology

NBER working paper 32894 makes the obvious point that felony convictions are a lifelong punishment. Employers do not want to hire ex felons and ex felons face real obstacles about where to live.

Noncarceral conviction is a common outcome of criminal court cases: for every individual incarcerated, there are approximately three who are recently convicted but not sentenced to prison or jail.

We develop an empirical framework for studying the consequences of noncarceral conviction by extending the binary-treatment judge IV framework to settings with multiple treatments.

We outline assumptions under which widely-used 2SLS regressions recover margin-specific treatment effects, relate these assumptions to models of judge decision-making, and derive an expression that provides intuition about the direction and magnitude of asymptotic bias when they are not met.

My words: the sentence below is key.

Under the identifying assumptions, we find that noncarceral conviction (relative to dismissal) leads to a large and long-lasting increase in recidivism for felony defendants in Virginia.

In contrast, incarceration relative to noncarceral conviction leads to a short-run reduction in recidivism, consistent with incapacitation.

While the identifying assumptions include a strong restriction on judge decision-making, we argue that any bias resulting from its failure is unlikely to change our qualitative conclusions. Lastly, we introduce an alternative empirical strategy, and find that it yields similar estimates.

Collectively, these results suggest that noncarceral felony conviction is an important and potentially overlooked driver of recidivism.