June 10

June 10

Markets and Stocks

The market is in good shape. All time highs typically bring more all time highs. AI will become integral to our lives. Try Google’s LM notebook assistant for free. GOOG is a great investment.

Broadcom reports Wednesday. I anticipate a great quarter.

Nvidia remains an attractive investment but I suggest waiting for a pullback before starting a new position. At the moment the price action is reminiscent of a slot machine.

Global governments are leaping into the AI spending boom says the WSJ.

Countries in Asia, the Middle East, Europe and the Americas are pouring billions of dollars into new domestic computing facilities for artificial intelligence, opening up a fast-growing source of sales for Nvidia and other tech companies.

Governments are boosting their budgets and brandishing other incentives to encourage local companies and multinationals to build new data centers and refit old ones with specialized computer chips, mostly from Nvidia. The goal: to develop AI locally and train large language models in their native languages, based on their own citizens’ data.

Driving the investments is a quest for more strategic self-reliance amid rising tensions between the U.S. and China that center on technology. Some countries are also seeking to safeguard their local culture—and their national security—in an AI-centric world after feeling they had been also-rans in the mobile-phone and cloud-computing revolutions.

Nvidia last month said so-called sovereign AI efforts are expected to bring in almost $10 billion this year, from nothing last year. The company reported $26 billion in quarterly revenue, nearly half of which came from big cloud-computing companies that are renting access to its chips.

Private equity is coming for sports on a global basis. The Premier League of England is a prime target.

Barron’s explains: in England , they are sounding the alarm, “The Americans are coming!” Wealthy Yanks now control or own significant slices of half of Britain’s 20 Premier League teams (the nation’s top soccer conference), including a number with ties to investment firms.

The index has now gone 328 trading days without a 2% one-day decline, its third-longest such streak this century, says Santoli on CNBC.

And on the surface, there is a stolid calm that suggests a system in comfortable equilibrium, the market achieving a kind of homeostasis. Four of the past five days last week, the S&P 500 moved less than 0.2%. The fifth day, Wednesday, kicked in the bulk of the week’s 1.3% gain. The CBOE Volatility Index finished back near the 12 level that has defined a recent floor not previously seen since the carefree moment before the Covid pandemic.

Thursday saw some $80 billion in Nvidia common stock turn over, well over 10-times the activity in comparably sized Apple and Microsoft. Perhaps this was peak fever, the record date for the 10-for-1 stock split that takes effect Monday? It’s more guess than analytical assessment.

No doubt, overall volumes in marginal sub-$1 stocks has soared in recent weeks, and retail options activity continues to break records. But it hasn’t become pervasive or indiscriminate, and while overall investor flows into equities have picked up, they are still outpaced by the sums going into money-market vehicles.

The S&P 500 is up almost 2% since its closing peak at the end of the first quarter, perhaps the moment of maximum belief in a seamless soft economic landing. The equal-weighted version, however, is 3.4% below its March 28 crest.

Bespoke Investment Group last week noted the index had hit its latest new high with the 10-day tally of advancing-vs.-declining stocks negative. It’s the kind of thing that can be made to sound a bit ominous, and no doubt more inclusive rallies tend to be better forward-looking signs of health than narrow ones.

But the prior 17 times the index hit a new 52-week high with similarly poor breadth, future returns going out several months were a touch better than average.

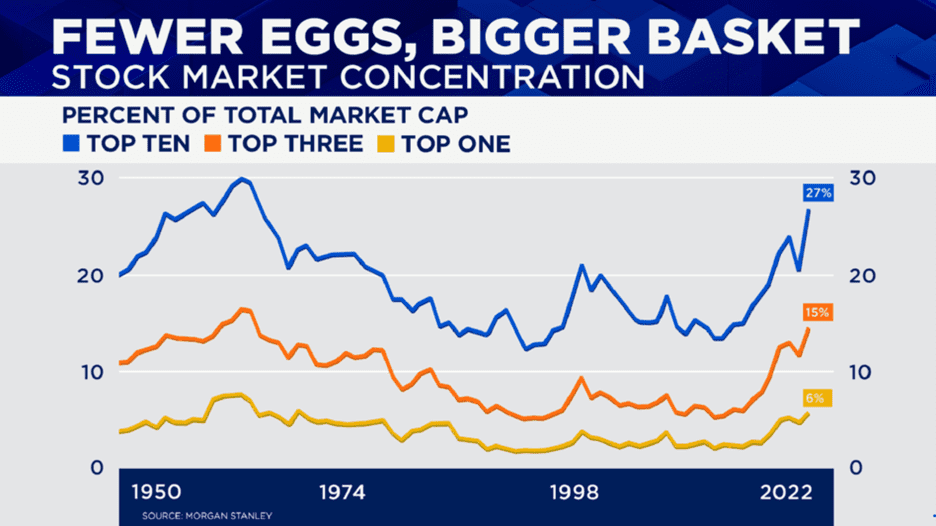

Three stocks together now account for fully 20% of the S&P 500 market value, mocking the notion of diversification and dashing most active investors’ hopes of beating the bogey.

Michael Mauboussin, longtime finance researcher, professor and investor now affiliated with Morgan Stanley Investment Management, released a thorough look at stock-market concentration through time, arriving at some interesting conclusions. One is simply that there have been similarly top-heavy markets in the past, which did not always result in poor subsequent performance. Note the early 1960s in this chart (which has data through the end of 2023).

Still, while there is no single “correct” way for markets to behave, the circumstances under which other groups pick up the slack would probably fit best with the current bull case: continued disinflation that allowed the Fed to trim rates in a deliberate way as the economy held firm and, presumably, the AI excitement kept animal spirits flowing.

This week we get: Apple’s hotly anticipated developers event where its AI strategy will be detailed, with the stock at the exact top of its one-year range, where it peaked twice before.

Another CPI report to see if the “sticky inflation” or “normalization” camps hold sway.

And a Fed meeting, with an updated collective projection of monetary policy, as the central bank approaches a full year with rates on hold at the presumed cycle high.

Economics

Dallas Fed working paper estimates the causal impact of government-funded R&D on business-sector productivity growth.

Identification is based on a novel narrative classification of all significant postwar changes in appropriations for R&D funded by five major federal agencies.

Using long-horizon local projections and the narrative measures, we find that an increase in appropriations for nondefense R&D leads to increases in various measures of innovative activity, and higher productivity in the long run.

We structurally estimate the production function elasticity of nondefense government R&D capital using the SP-IV methodology of Lewis and Mertens (2023), and obtain implied returns of 150 to 300 percent over the postwar period.

The estimates indicate that government-funded R&D accounts for about one quarter of business-sector TFP growth since WWII, and generally point to substantial underfunding of nondefense R&D.

https://www.dallasfed.org/research/papers/2023/wp2305

See also Marginal Revolution.

The public wants Social Security and Medicare but the public doesn’t want to pay the full cost of those income transfers. Politicians want to be re-elected. So, the federal government finances entitlements and not much else. No wonder economic growth is so slow. I sure hope AI delivers the goods.

Politics

The purpose of the United States is liberty. When government allocates our resources, at the margin liberty is denied. Under Biden government grows and liberty withers.

George Will of the Washington Post is right ! President Biden’s Administration is the most “progressive” in the history of the United States. Will writes:

The million-barrel release (one-ninth of the nation’s average daily use) will have no noticeable effect on prices.

It is, however, congruent with President Biden’s “whole of government” approach not only to promoting his reelection, but also to the progressive agenda of swarming American life with government.

Beyond serial student loan forgiveness, marijuana liberalization and multiple other mini-panders, Biden can truthfully boast that he has provided the most progressive governance in U.S. history.

Two defining characteristics of progressivism are: the goal of minimizing the market’s role by maximizing government’s role in allocating society’s resources and opportunities.

And confidence that the world is plastic to progressive government’s touch, and the future is transparent to progressives’ gaze.

The “shock” is the gift that keeps giving progressives an excuse to socialize the economy through government “partnerships.”

While denouncing “tax breaks” for “Big Pharma” and “Big Oil,” Biden (notes the Cato Institute’s Chris Edwards) favors trillions of dollars for “Big Semiconductor, Big Wind, Big Solar, Big Battery, Big Automaker, Big Utility.”

Automakers are now public utilities, whose future investments and product decisions are dictated by government. Twenty-first-century progressives preserve the shell of the (formerly) private sector as government’s appendage, but any vestiges of private autonomy are subordinated to the “existential” urgency of decarbonizing, which makes everything the government’s concern.

During the past three decades, Sharma says, the federal government, under both parties, eliminated a total of just 20 rules, while adding about 3,000 a year. Biden 2.0 would make matters even worse than would Trump 2.0, but it sometimes takes an ideological micrometer to measure the difference between today’s competing statisms.

https://www.washingtonpost.com/opinions/2024/06/07/biden-progressive-presidency/

The New Republic says: Every six months or so, we seem to pass through another phase of revelations that underscore the extent to which officials misled the public about the evidence concerning Covid-19’s origins and the protocols established to mitigate the virus’s spread.

While the political world has been fixated on Donald Trump’s legal battles these past several weeks (we’re no exception), some of the most damning pandemic-policy revelations yet have emerged. These, on the origins not just of Covid but of the guidance that upended society — kids’ education, people’s livelihoods, families and our relationships with each other.

The prior round of honest Covid reflection yielded a mea culpa of sorts from former NIH head Francis Collins, who last year acknowledged that public-health officials took a “narrow view” in decision-making, attaching “infinite value to stopping the disease and saving a life” and “zero value to whether this actually totally disrupts people’s lives, ruins the economy, and has many kids kept out of school in a way that they never quite recover from.” That mindset, he said, was “unfortunate” and a “mistake.”

The information emerging since might feel cathartic to those who faced scorn and ridicule for questioning Covid protocols or the “wet market” narrative. But really, it’s just maddening.

There was no science behind the six-feet rule for social distancing, there was no science justifying the masking of children, and the notion of the pandemic stemming from a lab leak wasn’t implausible or a conspiracy theory.

See National Review. For full disclosure I rarely pay attention to the National Review. It is too far right for me. But on the topic of Covid, NR is spot on especially with regard to the irreparable damage done to so many children.

I want to know the death rate for healthy adults over the age of 70 without underlying conditions and who were not obese. I still recall the data from the first cruise ship where Covid spread, 4 deaths among over 1,000 passengers most of whom were very elderly.